- Contact Us Now: (703) 558-9311 Tap Here To Call Us

Can a Trust Protect My Assets From Lawsuits or Creditors in Virginia?

Many Virginia families, professionals, and business owners ask whether a trust can protect their home, business, bank accounts, or investments from lawsuits and creditors. The question usually comes from a reasonable concern: people want to know whether a trust can serve as a legal shield. The answer is not simply yes or no. It depends on the kind of trust, the rights and benefits the settlor keeps, the timing of the transfer, and the risk the client is trying to address. A trust may be part of an asset protection plan. But a trust is not automatically a shield that protects everything from every lawsuit, creditor, business risk, or future problem.

A Common Question: “Can I Put Everything in a Trust So No One Can Touch It?”

I hear this question often. A potential client may say, “I want to create a trust and put my house, bank accounts, and business interests into it so they are protected if I ever get sued.” Others ask, “Can I put everything into a trust so creditors cannot reach it?” The concern is understandable. The misunderstanding is assuming that any trust automatically creates creditor protection. Some trusts are mainly estate planning tools. Some may provide creditor protection if properly structured. Some asset protection tools are not trusts at all.

The right answer depends on the goal.

Key Takeaways

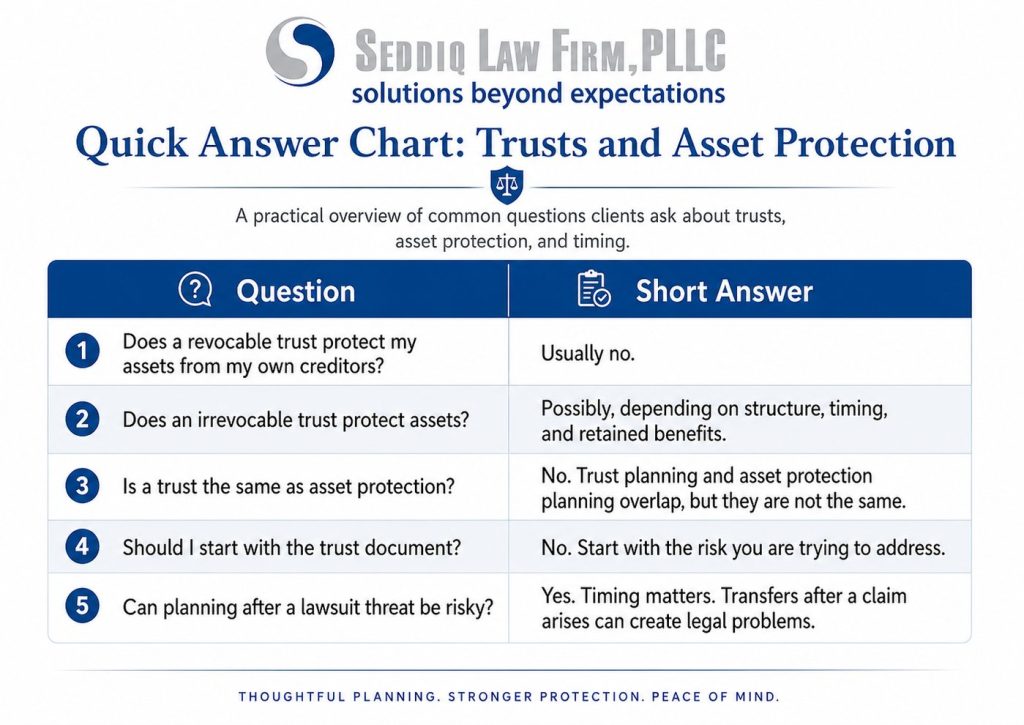

- A revocable living trust usually does not protect your own assets from your own creditors during your lifetime.

- In Virginia, property of a revocable trust is subject to claims of the settlor’s creditors during the settlor’s lifetime.

- An irrevocable trust may provide more protection, but retained benefits, distribution rights, timing, and statutory structure matter.

- Asset protection is usually layered planning, not a single document.

- The better question is not “Do I need a trust?” It is “What risk am I trying to address?”

The Legal Starting Point: A Revocable Trust Is Usually Not a Lawsuit Shield

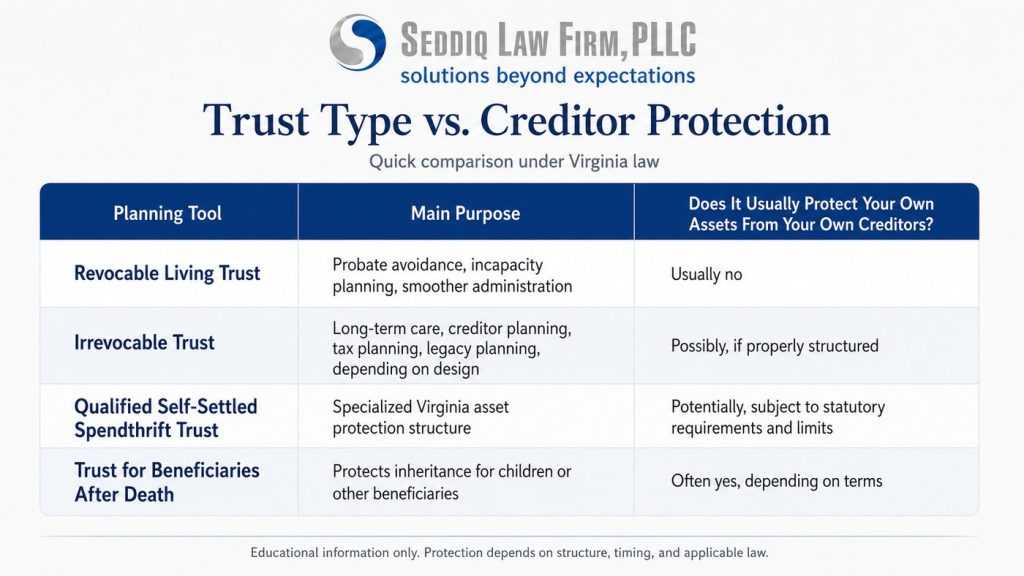

The most common estate planning trust is a revocable living trust. It can help avoid probate, organize assets, plan for incapacity, and make administration easier after death. But in Virginia, a revocable trust generally does not protect your assets from your own creditors during your lifetime. Under Virginia Code § 64.2-747(A)(1), during the lifetime of the settlor, the property of a revocable trust is subject to claims of the settlor’s creditors.

In plain English: if you create a revocable trust, fund it with your assets, and keep the power to revoke or amend it, those assets are generally still reachable by your own creditors during your lifetime. That rule makes sense because a typical revocable trust allows the settlor to revoke or amend the trust, serve as trustee, use the trust assets, move assets in and out, and change beneficiaries. A revocable trust may be excellent for probate and incapacity planning. It usually does not make a home, bank account, or investment account untouchable during the settlor’s lifetime.

Why Create a Revocable Trust If It Does Not Protect Assets From Creditors?

Because creditor protection is not the only reason to create a trust. A revocable trust may still help Virginia families avoid or reduce probate complications, plan for incapacity, keep administration more private than probate court, and organize how assets pass after death. The problem is not the revocable trust. The problem is expecting the revocable trust to do something it was not designed to do.

If the goal is probate avoidance, a revocable trust may be appropriate. If the goal is creditor protection, the analysis needs to shift to asset protection planning.

What About Irrevocable Trusts?

An irrevocable trust may provide stronger asset protection than a revocable trust, but “irrevocable” does not automatically mean “protected.” The legal question is more specific: what rights, benefits, powers, and interests does the settlor retain? For an irrevocable trust, Virginia Code § 64.2-747(A)(2) provides that, except as otherwise provided in Virginia’s self-settled spendthrift trust statutes, a creditor or assignee of the settlor may reach the maximum amount that can be distributed to or for the settlor’s benefit.

That is why retained benefit matters. If an irrevocable trust allows distributions back to the settlor or for the settlor’s benefit, creditor protection may be limited to the extent of that retained beneficial interest.

Virginia also recognizes a specialized planning structure called a qualified self-settled spendthrift trust. Under Virginia Code § 64.2-745.1, a settlor may transfer assets to a qualified self-settled spendthrift trust and retain a qualified interest, subject to statutory requirements and limitations.

This is not a casual form-document strategy. Virginia’s framework includes technical requirements, including irrevocability, qualified trustee requirements, Virginia-law requirements, a spendthrift provision, and limits on retained rights. See Virginia Code § 64.2-745.2.

An irrevocable trust may be part of an asset protection plan, but protection depends on the trust terms, retained benefits, timing, funding, trustee structure, and applicable Virginia law.

Timing Matters: Asset Protection Is Usually Proactive

Asset protection planning is strongest when it is done before a claim or lawsuit arises. If someone is already facing a lawsuit, has received a demand letter, is in default, owes significant creditors, or transfers assets after a known problem appears, the legal analysis changes.

Virginia law addresses transfers made with improper creditor-related intent. Under Virginia Code § 55.1-400, certain transfers made with intent to delay, hinder, or defraud creditors, purchasers, or other persons may be void as to those persons.

Virginia’s qualified self-settled spendthrift trust statute also preserves creditor remedies in certain circumstances, including where a transfer may be set aside on other bases, such as if the transfer renders the settlor insolvent, and for certain existing-creditor claims within the statutory period.

Asset protection should not be treated as a last-minute escape plan. The better approach is proactive, lawful planning based on a real risk analysis.

Start With the Goal, Not the Tool

When someone asks, “Can a trust protect my assets?” the better question is: what concern is driving the question?

Probate, incapacity, business liability, professional liability, rental property exposure, long-term care costs, beneficiary protection, privacy, and tax planning are different concerns. They may require different tools.

A person worried about probate may need a revocable trust. A business owner worried about company liability may need entity planning, insurance, and contracts. A physician worried about malpractice exposure may need professional liability coverage, umbrella coverage, titling review, and estate planning. A family worried about a child’s inheritance may need continuing trusts for beneficiaries.

The mistake is assuming one trust solves every problem.

A Trust May Be Part of the Answer, But It Is Not the Whole Answer

For many clients, asset protection is layered. The plan may involve estate planning documents, trusts, insurance, business entities, contracts, titling decisions, beneficiary designations, retirement account planning, long-term care planning, and business succession planning.

The right combination depends on the assets, risks, family situation, and timing. Planning should begin with what the client owns, what the client is worried about, and what the client wants to accomplish—not with a single document.

Bottom Line

A revocable living trust can help with probate avoidance, incapacity planning, privacy, and family administration. But under Virginia law, property of a revocable trust is generally subject to claims of the settlor’s creditors during the settlor’s lifetime.

An irrevocable trust may provide more protection, but the analysis depends on retained benefits, distribution rights, timing, funding, trustee structure, and statutory requirements.

If the concern is asset protection, the question is not simply whether a trust is needed. The question is what risk needs to be addressed and what legal tool actually addresses that risk.

Ready to Understand What Your Trust Can—and Cannot—Do?

Whether you are a healthcare provider, business owner, professional, or family trying to protect what you have built, the right plan starts with clarity. A trust may be part of the answer, but asset protection depends on your goals, your assets, your risk profile, and the structure of the plan.

Seddiq Law Firm helps Virginia families, professionals, and business owners understand the difference between estate planning, probate avoidance, and asset protection planning—so your documents match the risks you are actually trying to address.

Call (703) 558-9311, email info@seddiqlawfirm.com, or click here to contact us to schedule a consultation and bring clarity to your plan before small gaps become larger risks.

FAQ

Does a revocable trust protect assets from lawsuits in Virginia?

Usually no. Under Virginia Code § 64.2-747(A)(1), during the settlor’s lifetime, property of a revocable trust is subject to claims of the settlor’s creditors.

If I put my house in a trust, can creditors still reach it?

If the house is in a revocable trust and the settlor retains control, the trust usually does not protect the house from the settlor’s own creditors during the settlor’s lifetime.

Does an irrevocable trust protect assets from creditors?

It may, depending on the structure. For irrevocable trusts, Virginia law focuses in part on the maximum amount that can be distributed to or for the settlor’s benefit, except as otherwise provided by Virginia’s self-settled spendthrift trust statutes.

What is a qualified self-settled spendthrift trust in Virginia?

It is a specialized irrevocable trust structure recognized under Virginia law that may allow a settlor to retain a qualified interest while receiving certain creditor protection benefits, subject to statutory requirements and limitations.

Can I create a trust after I am threatened with a lawsuit?

That can be risky. Transfers made after a claim arises may be challenged under creditor protection and fraudulent transfer principles. Asset protection planning is strongest when done proactively.

What is the best way to protect assets?

There is no single best tool. Depending on the situation, a plan may involve insurance, trusts, LLCs, contracts, titling, retirement account planning, and business succession planning.

Legal Sources Referenced

- Virginia Code § 64.2-747 — Creditor’s claim against settlor

- Virginia Code § 64.2-743 — Spendthrift provision

- Virginia Code § 64.2-744 — Exceptions to spendthrift provision

- Virginia Code § 64.2-745.1 — Self-settled spendthrift trusts

- Virginia Code § 64.2-745.2 — Definitions related to qualified self-settled spendthrift trusts

- Virginia Code § 55.1-400 — Void fraudulent acts; bona fide purchasers not affected

Disclaimer: This article is for general informational purposes only and does not create an attorney-client relationship. Asset protection and trust planning are fact-specific and should be reviewed with counsel based on your circumstances.